.jpg)

Introduction

As of January 1, 2026, Aruba will introduce several important tax reforms aimed at increasing transparency, supporting economic growth, and making Aruba more attractive for businesses and skilled professionals. The changes focus on fringe benefits, expatriates, urban redevelopment, and start-ups in key sectors.

Below is a practical overview of what you need to know. Please feel free to contact us for any additional details and/or support.

Minimum Wage Reform

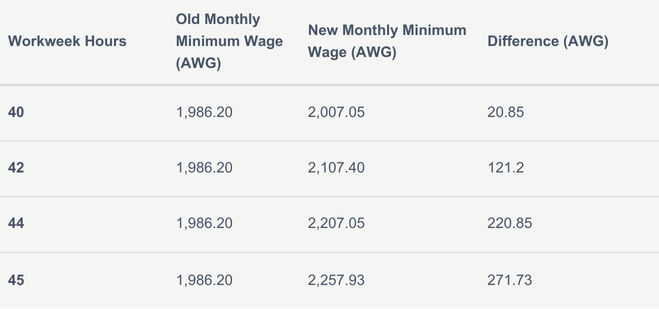

As of January 1, 2026, the calculation method related to the minimum wage will be adjusted as follows.

Minimum Hourly Wage

- AWG 11.58 per hour for employees aged 18 and older remains unchanged, however

- Monthly wages will now be calculated using 4.333 weeks per month, instead of 4.28 as previously according to DAO (Directie Arbeid en Onderzoek).

- This correction ensures a more accurate conversion from hourly to monthly wages.

Impact on employees

Employees working 40 to 45 hours per week will see an increase in their gross monthly salary, even if their hourly rate remains the same, especially in the industry that has a workweek of more than 40 hours.

Wage comparison

Higher Premium Contributions (AOV/AWW & AZV)

With the increase in the minimum wage, social security and health insurance premiums (AOV/AWW and AZV) will also increase for both employers and employees.

Example (45-hour workweek):

- Employer cost increases by AWG 324.45 per month.

- Employee contribution increases by AWG 17.94 per month.

Employer's Cost

Employee's Contribution

Tax Reforms Effective January 1, 2026

In addition to the minimum wage increase, the government has announced several tax reforms aimed at transparency, economic growth, and investment stimulation.

Fringe Benefits Regulation

The Fringe Benefits Regulation has been updated to provide:

- Clearer rules for company cars, housing, allowances, bonuses, and mobility reimbursements.

- Updated calculation to determine the fringe benefits, including incentives for electric and hybrid vehicles.

- Stricter anti-abuse measures to prevent improper tax-free benefits.

Company Cars

The taxable benefit is now calculated as 15% of the book value (to a minimum of 50% of the purchase price) of the car as of January 1 each year. To stimulate usage of hybrid and electric vehicles special rates applies:

- 10% for hybrid vehicles

- 5% for fully electric vehicles

Meals

Employers who provide meals must account for the value of the benefit in the employee’s taxable wage. These values have been updated to AWG 5 for breakfast and lunch, and AWG 7.50 for a hot meal.

Private Car Use For Business

For employees using their private car for business, the tax-free reimbursement increases to AWG 1.20 per business kilometer, provided proper mileage records are kept.

Tax-Free Relocation

The tax-free relocation and re-furnishing allowance has increased to AWG 20,000, giving employees and employers more flexibility.

Tax-Free Signing Bonus

In addition, for employees recruited from abroad, a tax-free signing bonus of up to one month’s salary (capped at AWG 10,000) can be paid within the first three months of employment.

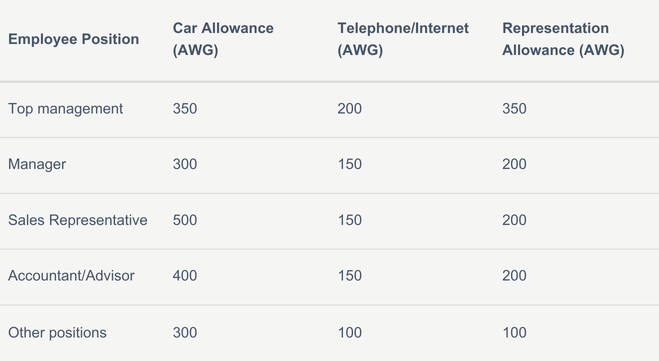

Tax-Free Monthly Allowances

Monthly allowances that can be granted tax-free based on position have been increased. Examples include car usage, representation costs, telephone and internet and a new category for employee health and well-being.

Service Anniversaries

Employees may receive tax-free amounts upon reaching service milestones:

Additionally, for each five-year milestone, employees may receive a maximum of AWG 500, and employers may grant a tax-free annual gift of up to AWG 400.

Business Travel

Expenses incurred for business trips, including accommodation, car travel, and daily allowances, are not included in taxable wages, as long as costs are reasonable. The daily allowance may be up to AWG 225 to cover incidental expenses during the trip.

Company Telephone

When the employer covers all telephone costs for an employee, part of this benefit is considered taxable. An annual amount of up to AWG 480 is added to the employee’s taxable wage. If the actual reimbursement is lower, only the reimbursed amount is included instead.

Employee Health and Well-Being

A new tax-free allowance of up to AWG 125 per month is introduced for employee health and well-being to cover expenses such as gym memberships and wellness programs.

Expatriate Regime

The expatriate regime has been expanded to make it easier for foreign professionals to qualify. Previously, only employees earning at least AWG 150,000 qualified. As of 2026, employees with:

- Higher professional education (HBO level), and

- have at least 5 years of relevant work experience, may also qualify, even if their salary is below AWG 150,000.

- Several allowance amounts within the regime have also been adjusted.

This reform supports Aruba’s goal of attracting skilled talent and diversifying its economy.

Economic Development Incentives

Oranjestad & San Nicolas

To stimulate urban renewal, Aruba is introducing a 10-year tax incentive program for redevelopment projects in Oranjestad and San Nicolas.

Key incentives include:

- Exemption from profit tax and dividend withholding tax from 2026 through 2035.

- Exemption from real estate transfer tax and turnover taxes (BBO/BAZV/BAVP) for 2026 and 2027.

These incentives apply to income and transactions directly linked to qualifying redevelopment projects. Strict conditions apply, including a minimum investment of AWG 500,000, and entities must be exclusively engaged in redevelopment activities. For projects that do not fully qualify, a flexible depreciation scheme of up to AWG 500,000 is available.

Start-up Policy

A new start-up policy aims to reduce tax pressure on newly established companies during their first five years to encourage innovation and entrepreneurship.

Eligible sectors include:

- Knowledge economy

- Agriculture

- Logistics

- Creative industries

- Circular economy

- Niche tourism

Incentives include:

- Profit tax exemption on profits up to AWG 50,000 per year.

- 20% investment allowance during the first five years.

- Tax deduction of up to AWG 30,000 per year on new business loans.

- Mandatory director’s salary aligned with the statutory minimum wage.

- Access to small entrepreneur turnover tax schemes.

Conditions apply, including reinvestment requirements, employment thresholds, and anti-abuse rules. If conditions are not met, benefits may lapse retroactively.

What Employers and Business Owners Should Do Now

- All businesses should be aware of compliance risks, as incorrect application of the new minimum wage calculation or fringe benefit valuation may result in penalties or retroactive corrections.

- Employers should reassess employee benefit structures to ensure compliance with the updated fringe benefit regulations.

- Reassess fringe benefit structures to comply with updated regulations

- Startups and investors should review the new tax incentive schemes early to determine eligibility and optimize tax planning.

Final Note

These reforms reflect Aruba’s strong financial position and its focus on sustainable growth, talent attraction, and entrepreneurship. While they offer opportunities, they also require careful planning and correct implementation.

PlusGroup can assist employers and entrepreneurs with payroll adjustments, tax planning, and compliance under the new rules.

Share insight

.jpg)